Songkran 2026: Inside Thailand's Biggest Holiday and What It Means for Brands

Songkran is Thailand's New Year festival — and one of Southeast Asia's most culturally distinct consumer moments. While the world may know it for its iconic water fights, what actually happens inside Thai households during this period tells a more nuanced story about spending priorities, family dynamics, and shifting generational attitudes.

Milieu Insight surveyed 500 Thai consumers in January 2026 to understand how they're approaching Songkran this year. For brands operating in or eyeing the Thai market, here's what the data reveals.

Most Thais Are Staying Close to Home

Travel behaviour this Songkran largely mirrors last year. The most common plan among respondents — chosen by 26% — is simply to stay home and rest, nearly identical to the 27% who said the same in 2025. It remains the single most-selected option.

Among those who do travel, plans are spread across short-distance options: around 25% plan to explore their own province, while 23% will return to their hometown in another province. Domestic cross-regional travel accounts for roughly 18%, and 19% remain undecided — a sign that a meaningful portion of consumers are still in a wait-and-see mode, or tend to plan close to the date.

One figure stands out at the top end: only about 3% plan to travel internationally, a slight uptick from 2% last year, but still a marginal share. Despite improved travel accessibility post-pandemic, Thais continue to favour domestic options during Songkran.

For travel and hospitality brands, this reinforces the case for doubling down on domestic packages rather than outbound promotions — and for targeting the undecided segment with timely, last-minute offers.

Songkran Is Family Time, Above All

When it comes to who Thais spend the holiday with, the answer is overwhelmingly family. 71% of respondents say they'll spend most of their time with family during Songkran — up from roughly 67% in 2025, cementing the festival's identity as a time for multigenerational reunion.

Other company is a distant second: around 10% will spend it with a partner, 8% with friends, and only 11% plan to spend the holiday alone.

This dominant family orientation has clear implications for brands. Campaigns that tap into intergenerational connection, family activity bundles, or group promotions are likely to resonate more strongly than those targeting individuals or peer groups. Travel packages, home entertainment products, and dining deals for groups of four or more are natural fits for this season.

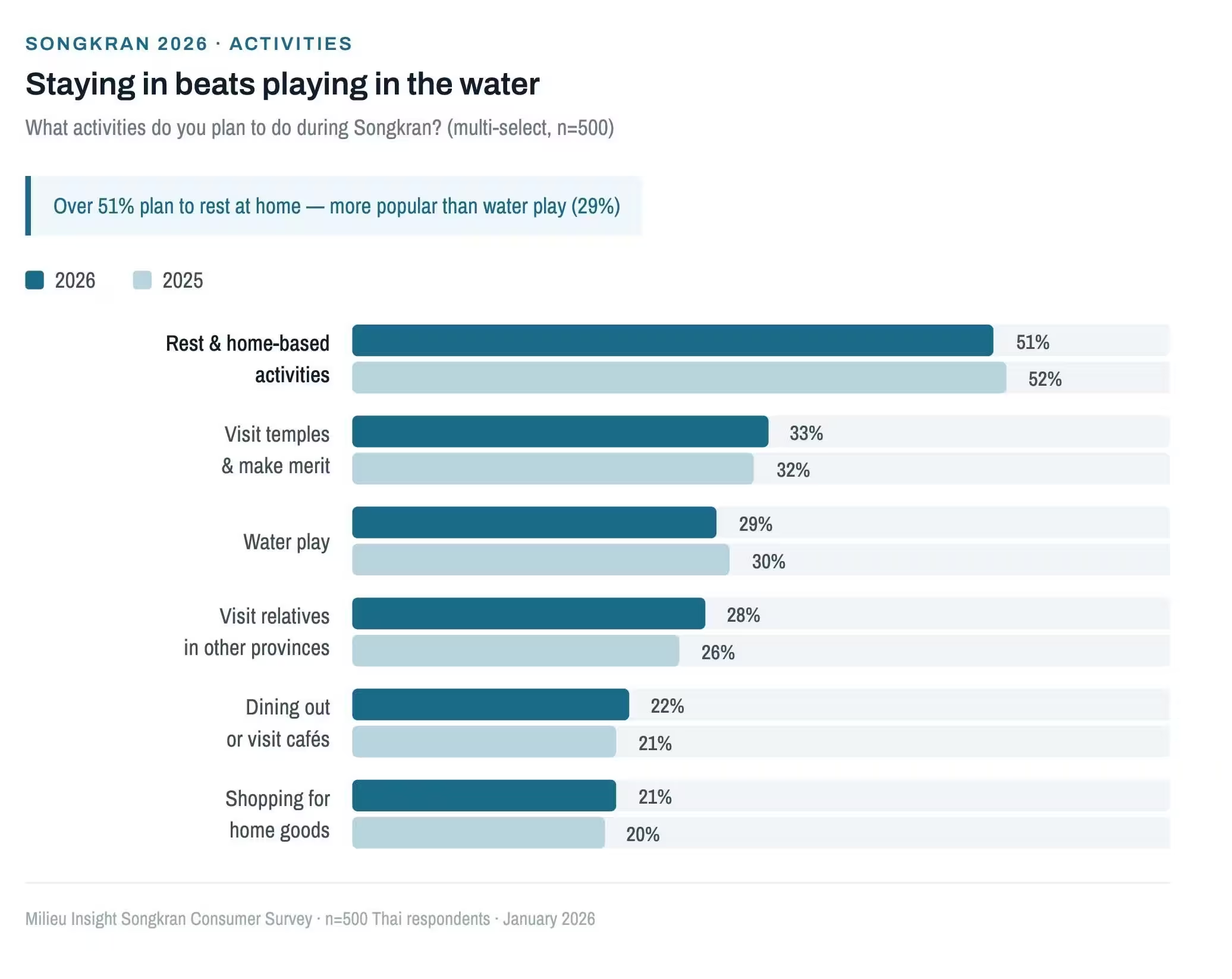

What People Actually Do: Staying In Beats Playing in the Water

Despite Songkran's global reputation as a water festival, the most popular activity among Thai respondents is actually staying home. Over 51% plan to rest and do home-based activities — watching content, playing games, or pursuing hobbies — consistent with the 52% who said the same in 2025.

The next most common activities are visiting temples and making merit (~33%) and water play (~29%). Other notable plans include visiting relatives in other provinces (~28%), dining out or visiting cafés (~22%), and shopping for home goods (~21%).

The preference for staying in reflects a combination of factors: the desire to recharge during a long break, the practical discomfort of outdoor activity in peak heat, and economic caution around travel expenses. For brands in home entertainment — streaming platforms, gaming, kitchen equipment, or DIY products — Songkran represents a genuine high-engagement window that tends to be underserved relative to its actual audience size.

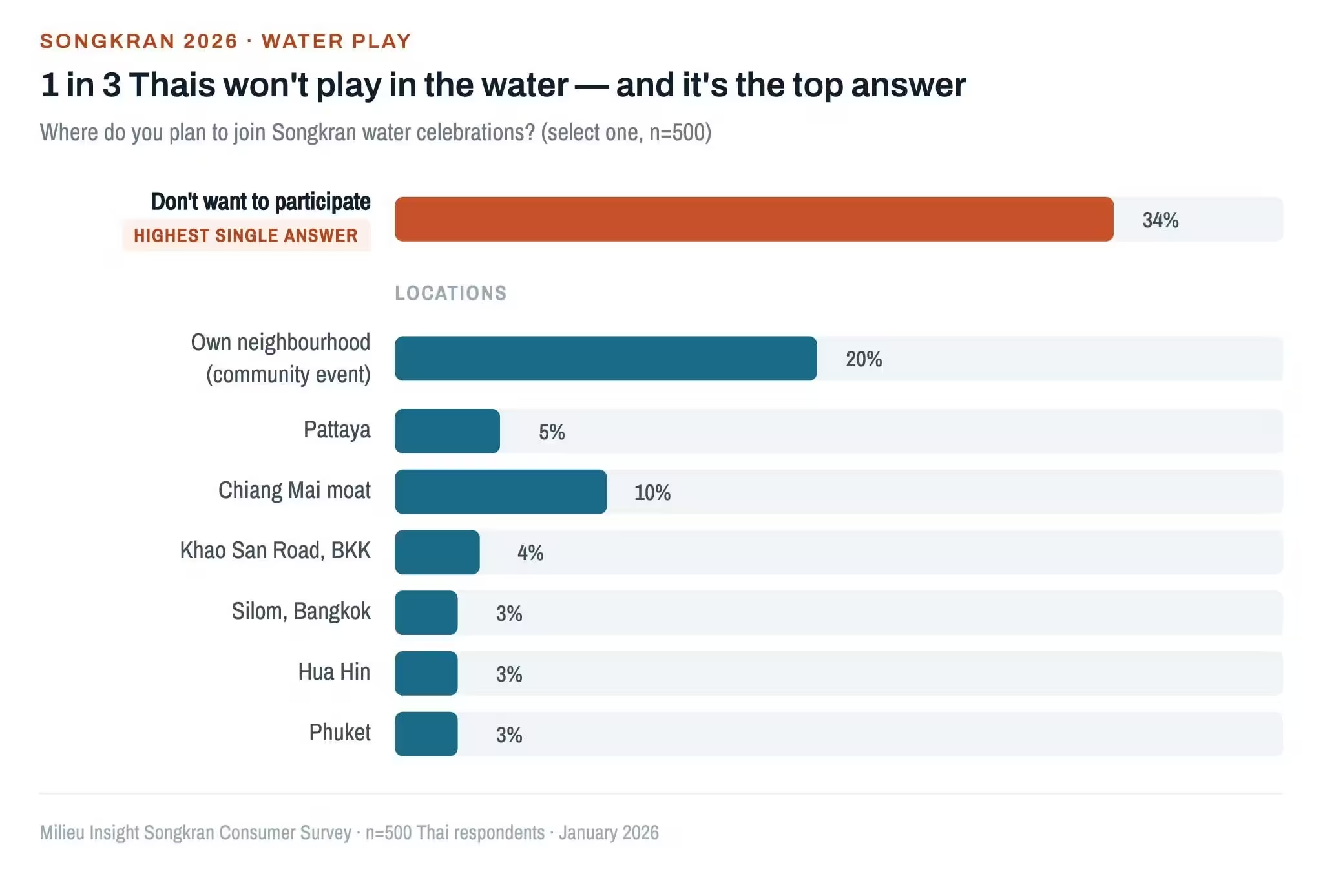

One in Three Thais Won't Play in the Water — And the Trend Is Generational

Perhaps the most striking finding for brands associated with Songkran's water-play tradition: 34% of respondents say they simply don't want to participate in water activities at all. This is the highest single response when respondents were asked where they plan to join Songkran celebrations.

Among those who do engage with water play, the most popular setting is community-organised events in their own neighbourhood (~20%) — not the famous tourist destinations. Well-known hotspots rank notably lower: Chiang Mai's moat (~10%), Bangkok's Khao San Road (~4%), Silom (~3%), and regional draws like Pattaya (~5%), Hua Hin (~3%), and Phuket (~3%) each attract only a small fraction.

Younger respondents aged 16–24 are the most likely to opt out of water play entirely, suggesting a generational shift in how Songkran is experienced. For brands that have traditionally anchored their Songkran activations to large-scale outdoor events, this is a signal worth noting. Localised community sponsorships and alternative programming — concerts, food festivals, charity runs — may better capture where attention is actually going.

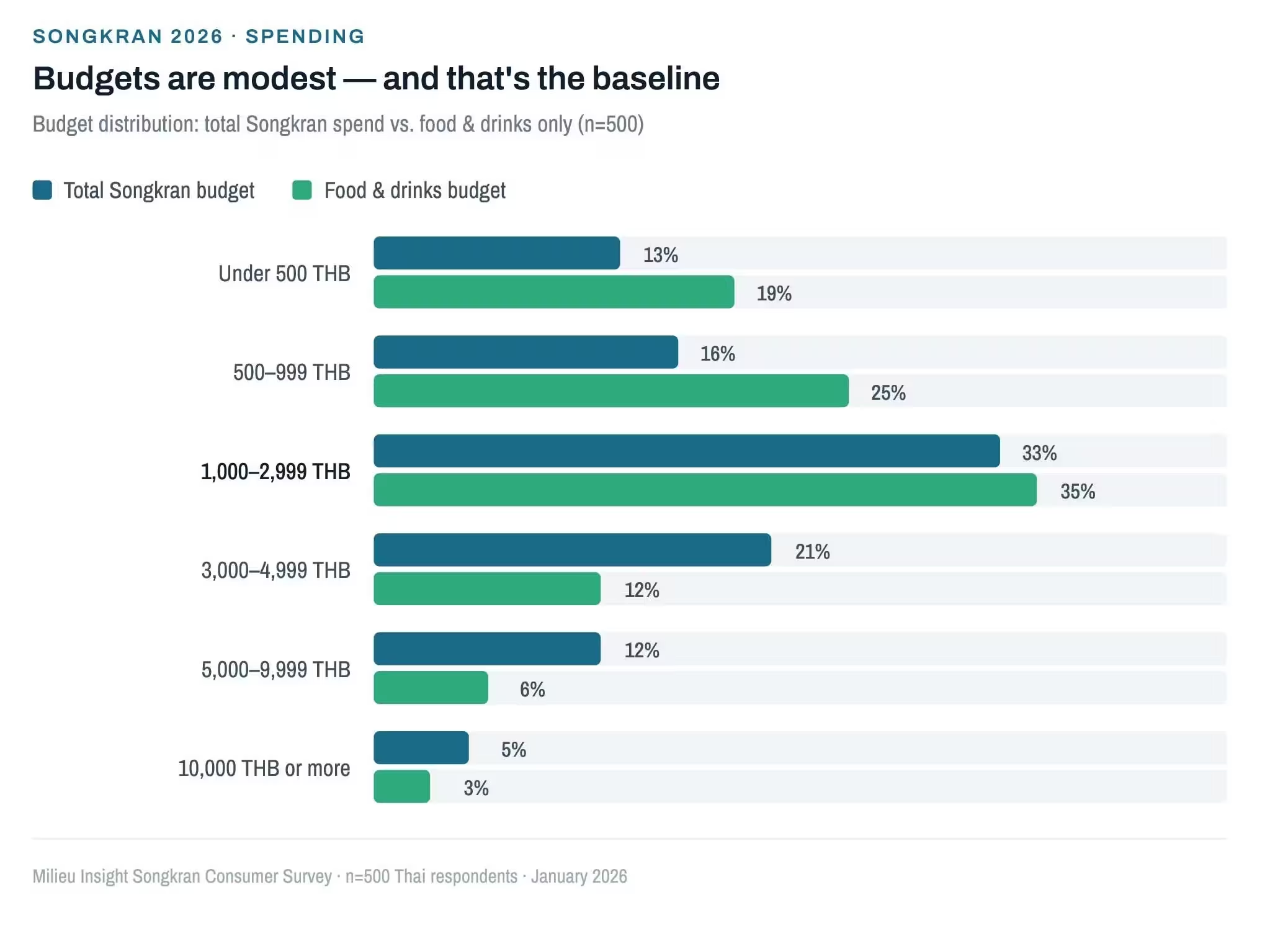

Budgets Are Modest — and That's the Baseline

Consumer spending during Songkran follows a cautious pattern that has remained stable year-on-year. The most common budget range for total Songkran spending (covering travel, shopping, dining, and celebrations combined) is 1,000–2,999 THB, cited by around 33% of respondents — similar to the 35% who indicated the same range in 2025.

The second-largest group sets aside 3,000–4,999 THB (~21%). On the more conservative end, ~13% plan to spend under 500 THB, while only ~18% in total plan to spend 5,000 THB or more (split roughly between 5,000–9,999 THB at ~12%, and 10,000 THB+ at under 6%).

Food budgets follow a similar distribution: most respondents (roughly 35%) allocate between 1,000–3,000 THB for food and drinks — consistent with the 37% at this level in 2025. Around 25% budget 500–999 THB for food, and 19% under 500 THB. Fewer than 20% plan to spend more than 3,000 THB on food alone.

The takeaway for brands is practical: pricing strategy and promotional mechanics matter more than premium positioning for most Songkran shoppers. Bundles in the 500–2,000 THB range, instalment-free promotions, and clearly communicated value are more likely to convert than aspirational messaging. Discounts, 0% instalments, and bonus-with-purchase mechanics can help edge cautious shoppers toward a decision.

Shabu, Seafood, and Soft Drinks: The Songkran Menu

Food choices during Songkran are as consistent as they are revealing. Shabu/BBQ/Moo Kata (Thai-style hot pot and grilled meat) holds the top spot at ~55% — unchanged from 2025, and likely to stay there. The format is inherently social: everyone gathers around the grill or pot, cooking together over an extended meal. It fits the family-reunion atmosphere of Songkran perfectly, even in hot weather.

Other staples round out the menu: seafood (~46%), northeastern Thai food such as som tum and laab (~44%), and soft drinks (~45%) as the essential cold beverage for a summer holiday. Alcoholic drinks are on about 29% of tables, while fried snacks (~37%) and desserts and cold sweets (~23%) also feature prominently.

Foreign or fast food is a lower priority: pizza, fried chicken, and burgers appear on around 21% of lists, while Japanese and Korean food sit at roughly 7%. Songkran leans Thai, leans communal, and leans toward dishes meant to be shared. For F&B brands, group-size formats — large BBQ sets, multipacks of cold drinks, family-portion seafood trays — are better aligned with actual demand than individual serving formats.

Where Thais Shop: Convenience Stores Lead, Fresh Markets Hold Strong

When it comes to stocking up for Songkran, convenience stores rank first, with 54% of respondents naming them as a go-to channel — driven by proximity, extended hours, and the reliability of staying open through public holidays when smaller shops close.

Hypermarkets (Lotus's, Big C, Makro) come in second at 51%, offering breadth of selection and Songkran-specific promotions on everything from water toys to household appliances to fresh food in bulk quantities.

The notable finding is how well fresh markets hold their own at ~49% — nearly level with hypermarkets. With many households cooking at home during Songkran, fresh ingredients sourced locally are a practical and cost-effective choice. Mid-size supermarkets like Tops and Foodland (~29%) retain their niche, while online delivery platforms (Grab, LINE MAN) reach around 20% — smaller, but meaningful for urban consumers who want convenience without leaving home.

The picture here is clear: physical channels dominate Songkran purchasing, and in-store visibility remains the most important lever for brands targeting this period. Point-of-sale positioning in convenience stores and hypermarkets before and during the holiday is essential. Reaching consumers through wet market supply chains is also worth considering for FMCG brands with appropriate distribution. Online delivery, while not the primary channel, can be activated effectively with holiday bundles and free-shipping mechanics for the stay-at-home segment.

What This Means for Brands

Songkran 2026 reinforces several consistent patterns in Thai consumer behaviour — with a few shifts worth watching:

This article draws on findings from Milieu Insight's Songkran 2026 Consumer Survey, conducted in January 2026 among 500 Thai respondents. For the full dataset, contact sales@mili.eu.

Author

Milieu Team

At Milieu, we’re a team of curious minds who love digging into data and uncovering what drives people. Together, we turn insights into stories—and stories into action. We also run on coffee, deadlines, and the occasional meme.

Latest Insights